Update2026.06.10 (수)

[Real Estate Collapse, AI Tax Nets, and Capital Controls: Fiscal Pressure Begins to Shake the Regime]

As the real estate-driven growth model that sustained the Chinese economy collapses, the Chinese government has begun leveraging new methods to secure revenue. Beijing is moving to drastically tighten its grip on individual asset tracking and overseas asset management through an AI-based digital tax system. Amid the compounding pressures of an economic downturn and capital flight, warnings are mounting that this fiscal crisis could transcend economic issues and spiral into a crisis of systemic trust in the regime. Today, the Chinese economy stands at a critical crossroads of structural transition, far beyond a simple growth slowdown.

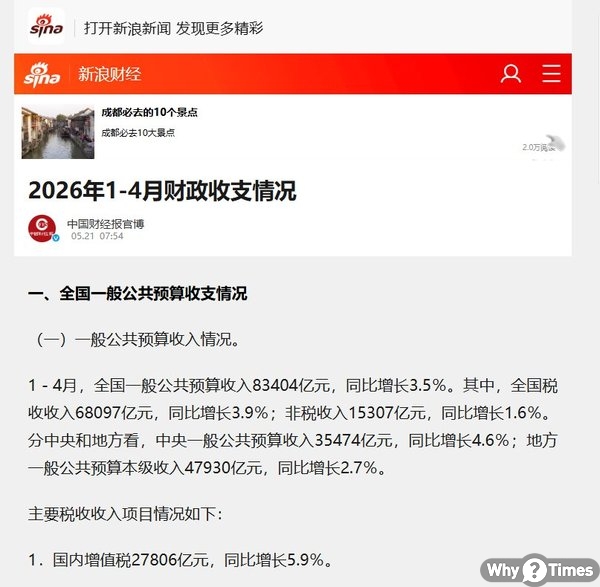

On May 21, China’s portal site Sina reported the fiscal revenue and expenditure data for the first four months of this year, as released by the Ministry of Finance. However, the official statistics contained a glaring anomaly. While total national fiscal revenue growth sputtered at just 3.5% year-on-year from January to April, personal income tax revenue surged by 12.2%. At a time when economic stagnation, corporate bankruptcies, and sluggish consumption are occurring simultaneously, the tax levied on individuals uniquely bucked the trend. In contrast, corporate income tax fell by 0.5% and consumption tax dropped by 3.3%. This serves as clear evidence that rather than raising tax rates, the state is forcibly extracting funds that previously remained hidden outside the tax net.

In 2025, China's personal income tax revenue reached 1.62 trillion yuan, an 11.5% increase from the previous year, and this upward trajectory persisted into the first quarter of 2026, rising 10.5% to 501.8 billion yuan. This reflects that even amid a broader macroeconomic downturn, the incomes of middle- and high-income earners are being captured and taxed more rigorously than ever before. These figures represent something far more significant than a mere increase in tax revenue; they signal that the government is not generating new wealth, but rather draining hidden private assets.

[The State Aggregates All Financial Data: The Reality of the AI Tax Surveillance Network]

The core tool driving this tax collection surge is a digital tax integration system that Chinese authorities have been building for years. Officially named "Golden Tax Phase IV" (金稅四期), it is, in simpler terms, a nationwide asset surveillance network that aggregates all individual financial data into a single hub for AI-driven analysis. Data held by the tax bureau, banks, public security, and the State Administration for Market Regulation are linked in real time. Bank transaction histories, securities account returns, platform earnings from e-commerce or YouTube, and even offshore accounts are cross-analyzed within this single system. Unlike previous generations that merely tracked tax invoices, the current system monitors capital flows in real time and automatically cross-checks corporate registration data with financial behavioral patterns.

Caixin, a Chinese economic media outlet and official partner of The Wall Street Journal (WSJ), reported:

"This system connects taxpayers, tax authorities, and policymakers into a single, vast digital platform, fundamentally transforming tax reporting practices. Income, stock incentives, and non-wage compensation that were previously shielded from regulatory scrutiny are now exposed with a single click."

Local tax officials have also publicly acknowledged that "revenues that previously sat outside the surveillance net have now been fully integrated into the tax base." The fifth-generation system, currently in its testing phase, aims to take this a step further: if reported income does not align with actual consumption and asset levels, it will introduce a method to retroactively calculate the "wealth the individual theoretically should possess" and levy taxes accordingly.

[Money Hidden Overseas Is No Longer Safe]

The most aggressive measures are targeted at] tracking overseas assets. China is a participant in the Common Reporting Standard (CRS), a global framework involving over 100 countries, allowing it to automatically receive offshore financial data. This means that even if an individual holds accounts in Singapore or Hong Kong, that information is flagged to Chinese tax authorities.

Bloomberg reported that "China is intensifying tax collection on its citizens' overseas income, broadening its focus from the ultra-wealthy targeted last year to now encompass middle-class professionals." The Hong Kong-based South China Morning Post (SCMP) also noted:

"Authorities are expanding overseas asset taxation beyond high-net-worth individuals to retail investors and middle-class professionals. Capital gains and dividends from overseas stock investments are subject to a 20% tax rate, with late fees applied for non-compliance."

The SCMP further highlighted that "Starting March 2026, a 'public shaming' mechanism was introduced to publish the names of delinquent taxpayers in the media, while crackdowns have intensified on tax evasion through offshore trusts holding Hong Kong-listed shares."

On May 22, an even more drastic measure came to light. Bloomberg reported that "China has launched an unprecedented crackdown on illegal cross-border transactions to stem capital flight, imposing severe penalties on popular brokerages and ordering the liquidation of non-compliant accounts within two years."

Bloomberg also noted that "The so-called 'hot money' (short-term speculative capital) that fled China over the course of 2025 was estimated at approximately $1 trillion, marking the largest capital outflow since data tracking began in 2006." The latest move to block offshore securities trading is an attempt to plug that exit. This effectively shuts down the final investment channel for a middle class that no longer trusts the domestic real estate market or onshore equities (A-shares).

[Why Now: The End of the Land-Dependent Era]

The driver behind this aggressive tax campaign and capital control regime boils down to one factor: the sharp plunge in land sales revenue, which has traditionally been the primary source of income for local governments. For the past two decades, Chinese local governments operated on a cyclical model where they 'sold land → developers built apartments → residents bought homes through loans.' With the collapse of the real estate market, this chain has broken.

The US-based think tank Rhodium Group diagnosed the situation:

"The most accurate description of China’s domestic economic weakness is not a crisis or a collapse, but a 'prolonged decay'—a gradual erosion of the efficiency and effectiveness of policy tools, which in turn weakens economic growth. The root of this lies in China's fiscal and financial systems."

Both the IMF and the World Bank have flagged these dynamics as warning signs. In early 2026, the IMF assessed the Chinese yuan to be 16% undervalued, applying pressure on Beijing for appreciation.

Meanwhile, Caixin analyzed that "The 2026 budget marks a historic shift, with public spending hitting a record 30 trillion yuan and the fiscal deficit ratio reaching 8.1%. The central government is consolidating fiscal responsibility, fundamentally altering the paradigm of local government-led growth." Simply put, as local governments have lost the ability to generate revenue independently, the structure has shifted to the central government issuing debt to plug the deficits.

[Cracks in Regime Legitimacy: The Greater Crisis Facing Xi Jinping]

An analysis that the economic crisis is expanding beyond a typical downturn into a crisis of legitimacy for the Xi Jinping regime has now become a consensus view among major foreign media outlets.

Foreign Policy warned:

"While official opinion polls continue to show high approval ratings for President Xi Jinping, discontent with his governance is intensifying across various social strata. The legitimacy of the Chinese Communist Party (CCP) is built on performance, not consent. If growth slows, jobs disappear, and housing prices fall, that legitimacy vanishes without any structural support."

Bloomberg similarly observed that "For decades, the CCP encouraged the narrative that legitimacy flows from delivering rapid growth, with Deng Xiaoping famously declaring that 'development is the only hard truth.' The Xi Jinping regime is now attempting to shift the center of gravity from growth toward a 'values-based legitimacy.'"

The Asia Society Policy Institute (ASPI) evaluated that "2026 serves as the political runway leading to the 21st Party Congress in 2027. Xi Jinping views this timeline as the ultimate benchmark to gauge whether his centralized governance model can sustain economic momentum and political legitimacy."

[A Vicious Cycle Eroding Economic Vitality]

Ironically, a paradox is taking hold: the aggressive tax collection and stringent capital controls deployed to overcome the fiscal crisis are draining economic vitality at an accelerated pace. Heavier tax burdens reduce consumer spending capacity, blocked capital channels dampen investment sentiment, and entrepreneurs prioritize asset protection over business investment—a structure that progressively weakens the momentum for economic recovery.

The Asia Society Policy Institute's Center for China Analysis (CCA) projected:

"If economic pressures intensify—such as a stock market crash, further plunges in housing prices, or a breakdown in tariff truces—Xi Jinping may be forced to inject greater pragmatism into his economic policies to protect the regime's legitimacy."

Government can collect more taxes. It can also restrict the movement of capital. However, it cannot force confidence in the future. The biggest crisis currently facing the Chinese economy is not a fiscal shortage, but rather the fact that trust in its growth model is shaking.

-중국 푸단대학교 한국연구원 객좌교수

-전 EDUIN News 대표

-전 OUR NEWS 대표

-제17대 대통령직인수위원회 정책기획팀장

-전 대통령실 홍보기획비서관

-사단법인 한국가정상담연구소 이사장

-저서: 북한급변사태와 한반도통일, 2012 다시우파다, 선거마케팅, 한국의 정치광고, 국회의원 선거매뉴얼 등 50여권